We use necessary cookies to make our site work (for example, to manage your session). We’d also like to use some non-essential cookies (including third-party cookies) to help us improve the site. By clicking ‘Accept recommended settings’ on this banner, you accept our use of optional cookies.

Necessary cookies

Analytics cookies

Yes

Yes

Yes

No

Necessary cookies

Necessary cookies enable core functionality on our website such as security, network management, and accessibility. You may disable these by changing your browser settings, but this may affect how the website functions.

Analytics cookies

We use analytics cookies so we can keep track of the number of visitors to various parts of the site and understand how our website is used. For more information on how these cookies work please see our Cookie policy.

Financial Stability in Focus: The corporate sector and UK financial stability

Financial Stability in Focus examines specific issues related to financial stability and sets out the views of the Financial Policy Committee of the Bank of England on these issues.

Banks are strong enough to continue to support households and businesses through the recovery from the pandemic.

Financial markets

There is evidence of heightened risk-taking in some financial markets, and vulnerabilities remain in the non-bank sector.

In focus: UK businesses

Businesses, particularly small firms, have increased their debt levels through the pandemic, but the financial system is strong enough to manage the risks this creates.

Published on

08 October 2021

Banks are strong enough to keep supporting UK households and businesses through the recovery from the pandemic

The UK economy is projected to recover further from the Covid pandemic over the remainder of the year. But risks to the recovery remain, particularly around how the economy will adjust as Government support, such as the furlough scheme, comes to an end.

The UK banking system is strong enough to continue to support households and businesses through the economic recovery. Major UK banks and building societies have been resilient to the challenges posed by Covid, and their capital and liquidity positions remain strong. It is important for banks to continue to lend to support viable, productive businesses. Maintaining the provision of finance can help businesses and the economy grow.

Businesses, particularly small firms, have increased their debt levels through the pandemic

The pandemic presented a large financial shock to UK businesses. Support from authorities – including the Government and Bank of England – and from the financial sector helped businesses to continue operating during the pandemic. Part of the support came in the form of government-backed lending to businesses.

Overall, the level of debt taken on by UK businesses has increased moderately during the pandemic. But there has been a larger increase in borrowing by small and medium-sized enterprises (SMEs). Many of these businesses had not previously borrowed.

A high level of debt among UK businesses can lead to risks to the financial system. Higher debt levels can cause businesses to cut back on employment and investment more in the face of economic shocks. This can have a negative impact on people’s jobs and incomes. Banks can also take losses if businesses struggle to pay back their loans.

The level of debt taken on by UK businesses has increased during the pandemic, especially among SMEs

The UK financial system is resilient to risks from the higher level of debt among UK businesses. The way these risks evolve will depend on how the economy recovers from the pandemic. We will continue to monitor these developments closely.

Our new series of publications – ‘Financial Stability in Focus’ – focuses on specific issues in depth and complements our Financial Stability Report, which is published twice a year. Risks linked to businesses are examined in this issue.

There is evidence of heightened risk-taking in some financial markets

Financial markets play an important role in supporting the economy and provide a substantial amount of finance to businesses. If financial markets do not function properly, businesses may be unable to raise funds through those markets.

There is evidence that investors are taking higher levels of risk in some global markets. For example, there are fewer protections in place when investors lend to companies with high levels of debt in so-called “leveraged loan” markets. And the prices of some financial assets appear high relative to historical norms.

We are monitoring these risks closely. We are also working with UK and other international authorities to make market-based finance more resilient to shocks, so that financial markets can support the economy in bad times as well as good.

Cryptoasset markets continue to grow rapidly, but currently pose limited risk to UK financial stability. Regulation needs to develop quickly enough, both domestically and at a global level, to address the risks they could pose in the future.

The Financial Policy Committee (FPC) aims to ensure the UK financial system is prepared for, and resilient to, the wide range of risks it could face – so that the system can serve UK households and businesses in bad times as well as good.

The outlook for financial stability

Support for the economy during the recovery

The UK financial system has provided support to households and businesses to weather the economic disruption from the Covid pandemic, reflecting the resilience that has been built up since the global financial crisis alongside the exceptional policy responses of the UK authorities.

UK GDP is projected to recover further over the remainder of the year towards its pre-pandemic level, although the outlook for the economy remains uncertain. The pace of recovery has slowed recently, and inflationary pressures have risen.

Households and businesses are likely to need continuing support from the financial system as the economy recovers and the Government’s support measures continue to unwind. The UK banking system has the capacity to continue to provide that support. The FPC continues to judge that the banking sector remains resilient to outcomes for the economy that are much more severe than the Monetary Policy Committee’s central forecast in the August Monetary Policy Report.

The FPC expects banks to use all elements of their capital buffers as necessary to support the economy through the recovery. It is in banks’ collective interest to support viable, productive businesses, rather than seek to defend capital ratios by restricting lending.

To support bank lending to households and businesses as the economy recovers, the FPC is maintaining the UK Countercyclical Capital Buffer (CCyB) rate at 0%. The FPC has previously stated that it expects to maintain a 0% UK CCyB rate until at least December 2021. It will re-evaluate the appropriate level of the UK CCyB rate in light of the risk environment at that time. In line with the standard implementation period, any subsequent increase would not be expected to take effect until the end of 2022 at the earliest.

The FPC will also consult on a proposal to change the metric used to determine Other Systemically Important Institutions (O-SII) buffer rates to exclude central bank reserves, effective from the 2023 Prudential Regulation Authority (PRA) assessment of individual firm buffer rates. The FPC also welcomes the PRA’s intention to continue to freeze O-SII buffer rates until that point. This will ensure that the increase in central bank reserves since the start of the pandemic will not result in higher regulatory capital buffers for banks before the FPC’s proposals can come into effect.

Domestic debt vulnerabilities

As the economy continues to recover, the FPC will remain vigilant to debt vulnerabilities in the financial system that could amplify risks to financial stability.

UK house price growth has reached levels last seen before the global financial crisis and housing market activity has been strong, reflecting a mix of temporary policy support and factors that could prove more persistent. Strength in the housing market has historically been associated with riskier lending practices. However, there is little evidence so far of a deterioration in lending standards or a material increase in the number of highly indebted households.

The FPC has Recommendations in place which limit a deterioration in mortgage underwriting standards or a rapid build-up in the share of highly indebted households. The FPC is due to finalise its review of the calibration of its mortgage market Recommendations in December 2021.

The FPC judges that UK corporate debt vulnerabilities have increased moderately over the Covid pandemic so far. The increase in indebtedness has not been large in aggregate, and debt servicing remains affordable for most UK businesses. Large increases in interest rates or severe earnings shocks would be needed to impair businesses’ ability to service their debt in aggregate.

The increase in debt in the UK corporate sector has been concentrated in some sectors and types of businesses, in particular in small and medium-sized enterprises (SMEs). Many of these SMEs had not previously borrowed and some would not have previously met lenders’ lending criteria. The increase in debt – though moderate in aggregate – has likely led to increases in the number and scale of more vulnerable businesses. As the economy recovers and government support, including restrictions on winding up orders, falls away, business insolvencies are expected to increase from historically low levels.

The FPC continues to judge that the UK financial system is resilient to risks from the UK corporate and household sectors. The FPC will monitor the evolution of vulnerabilities as the economy recovers and remains vigilant to risks building up over the medium term.

Global debt vulnerabilities

Debt vulnerabilities globally have also increased during the pandemic. Across advanced economies, corporate debt-to-GDP ratios have increased in aggregate by 10 percentage points since the end of 2019. Higher leverage and greater risk-taking abroad could directly increase the risk of losses for UK institutions on their foreign exposures. UK banks, however, have limited direct exposures to the most vulnerable sectors and so far debt servicing generally remains affordable. Corporate debt vulnerabilities in other countries could have more indirect spillovers to the UK.

Concerns about the ability of Evergrande Group, one of China’s largest property developers, to meet its financial obligations have been associated with recent volatility in international markets, and could pose risks to the wider property sector in China with potential spillovers internationally. The FPC has previously highlighted the risks associated with the rapid rise in debt more broadly in China and continues to monitor any of these potential risks to UK financial stability. While there is uncertainty as to how these risks might crystallise, the interim results of the 2021 Solvency Stress Test (SST) indicate that the UK banking system is resilient to the direct effects of a severe downturn in China and Hong Kong, and sharp adjustments in global asset prices.

Increased risk taking in global financial markets

The FPC judges there is evidence that risk-taking remains elevated in a number of markets relative to historic levels.

Following the Covid shock, central banks cut interest rates and undertook asset purchases to support economic activity and prevent an unwarranted tightening of financial conditions for corporates and households. Since then, risky asset prices have increased and, in a number of markets, asset valuations appear elevated relative to historical norms. This partly reflects the improved economic outlook, but may also reflect a ‘search for yield’ and higher risk‐taking in a low interest rate environment.

Asset valuations could correct sharply if, for example, market participants re‐evaluate the prospects for growth, inflation or interest rates. Any such correction could be amplified by vulnerabilities in market‐based finance that were exposed in March 2020. This could have consequences for market functioning and financial conditions, and hence the real economy.

Risks in leveraged loan markets globally continue to build. There are signs of continued loosening in underwriting standards and increased risk-taking in some investment banking businesses. These risks can affect UK financial stability through the direct impact on banks and the indirect impact of losses spreading through other parts of the global financial system. The core UK banking system is resilient to direct losses associated with leveraged lending, as demonstrated by the interim results of the 2021 SST.

Building the resilience of the financial system

Market-based finance

The March 2020 stress exposed a number of vulnerabilities in market-based finance. The FPC set out the next steps needed to enhance the resilience of market-based finance in July, and strongly supports the current work, co-ordinated internationally by the Financial Stability Board (FSB), to assess and remediate the underlying vulnerabilities. Such work is necessarily a global endeavour, reflecting the international nature of these markets and their interconnectedness. The Bank, the Financial Conduct Authority (FCA) and HM Treasury are fully engaged in this work programme, and the G20 will be updated on progress in October.

Until this work results in an increase in the resilience of non-bank financial institutions, the financial stability risks exposed in March 2020 will remain. And while central banks may need new and more targeted tools to deal effectively with financial instability caused by market dysfunction, central bank interventions cannot be a substitute for internationally co-ordinated reforms that enhance the resilience of the non-bank financial sector.

Cryptoasset and associated markets and services continue to grow and to develop rapidly. Such assets are becoming increasingly integrated into the financial system. The FPC judges that direct risks to the stability of the UK financial system from cryptoassets are currently limited. However, regulatory and law enforcement frameworks, both domestically and at a global level, need to keep pace with developments in these fast-growing markets in order to manage risks and to maintain broader trust and integrity in the financial system.

The FPC will continue to pay close attention to developments, including the relationship between cryptoassets and the UK financial system, and thereby seek to ensure resilience to systemic risks that may arise from further developments in cryptoasset markets. The FPC considers that financial institutions should take a cautious and prudent approach to any adoption of these assets.

Productive finance to support the economic recovery

The supply of finance including for productive investment is important both for financial stability and long-term growth and can help to support the recovery from the pandemic. The FPC welcomes the Productive Finance Working Group’s final report, which sets out the case for long-term investment via a ‘Long-Term Asset Fund’ (LTAF) vehicle, and recommendations to help make progress on removing barriers to investment in less liquid assets.

Understanding how the provision of finance to SMEs is developing is important for the FPC’s understanding of the vulnerabilities associated with SME indebtedness and for the FPC’s secondary objective, but is impaired by data gaps. The FPC welcomes the upcoming Bank survey on UK businesses’ financing decisions, which will seek to address some of these gaps.

Libor transition

Most Libor benchmarks, as well as new use of any continuing Libor benchmarks, are due to stop by the end of 2021. The FPC welcomes the progress that has been made so far in transitioning away from Libor and the marked increases in use of risk-free rates over recent months, in particular the recent positive progress in the transition to the Secured Overnight Financing Rate (SOFR) in US dollar markets. SOFR-based rates provide more robust alternatives than the credit sensitive rates that have begun to be used in some US dollar markets. The FPC emphasises that market participants should use the most robust alternative benchmarks available in transitioning away from use of Libor to minimise future risks to financial stability.

Critical third parties

The increasing reliance by the financial system on critical third parties (CTPs), including cloud service providers, can bring benefits to the financial sector, including improved operational resilience. However, the increasing criticality of the services that CTPs provide, alongside concentration in a small number of providers, pose a threat to financial stability in the absence of greater direct regulatory oversight.

Regulated firms will continue to have primary responsibility for managing risks stemming from their outsourcing and third-party dependencies. However, additional policy measures, some requiring legislative change, are likely to be needed to mitigate the financial stability risks stemming from concentration in the provision of some third-party services. These policy measures should include: an appropriate framework to designate certain third-party service providers as critical; resilience standards; and resilience testing. The FPC supports the intention of the Bank, PRA and FCA to publish a joint Discussion Paper in 2022 on these issues.

The FPC strongly supports UK financial authorities’ continued engagement with initiatives by the UK Government to strengthen cross-sectoral oversight of third-party service providers to multiple parts of the UK’s critical infrastructure, as well as in international workstreams at the FSB and other bodies, and with overseas financial regulators.

In focus – The impact of the Covid pandemic on corporate sector vulnerabilities

The Financial Stability in Focus (FSIF) sets out the Financial Policy Committee’s (FPC’s) view on specific topics related to financial stability. It complements the Financial Stability Report, which is published twice a year.

The Covid-19 (Covid) pandemic and the measures taken to contain it have had a significant and uneven impact on UK businesses. This FSIF provides a detailed assessment of how the Covid pandemic has affected businesses’ balance sheets and the implications for UK financial stability.

Consistent with its primary objective of supporting financial stability, the FPC seeks to ensure any build-up of debt vulnerabilities in the corporate sector does not pose risks to the wider financial system, which could ultimately undermine the ability of the financial system to serve UK households and businesses in bad times as well as good. Prior to the Covid pandemic, the FPC judged that the UK corporate sector posed limited risk overall to UK financial stability, although there was a sizeable tail of highly leveraged companies and potential fragilities in financial markets which could affect the provision of finance to companies. This judgement reflected both that debt levels were affordable in a low interest rate environment, and the high degree of resilience of UK banks.

The pandemic presented a substantial shock to UK businesses. Actions by UK authorities – including the Government and the Bank of England – and support from the financial sector has helped many businesses bridge the disruption. Part of that support came in the form of government-guaranteed loan schemes. While aggregate debt in the UK corporate sector has increased moderately over the Covid pandemic so far, that increase in debt has been concentrated in some sectors and types of businesses – in particular, small and medium-sized enterprises (SMEs), many of which had not previously borrowed. This increase, though moderate in aggregate, is likely to have increased the number and scale of more vulnerable businesses.

Debt servicing remains affordable for most businesses, and large increases in the cost of borrowing or severe earnings shocks would be needed to impair businesses’ ability to service their debt in aggregate. But within this aggregate picture it is likely that some companies will face challenges, for example if their business models are less able to adapt to structural change or if their debts levels were already high. SMEs are more likely to face particular financial pressures as they have been disproportionately impacted by the pandemic, and have increased their debt more than larger companies. However, much of this debt has been issued at low interest rates that are fixed for initial periods of up to six years which will limit the burden on businesses.

As the economy recovers and government support – including the ban on winding-up petitions –unwinds, business insolvencies are expected to increase from historically low levels. Risks from distress to businesses for the UK banking sector have been considered as part of the 2021 Solvency Stress Test. Three factors help mitigate direct risks to bank resilience: (i) most new bank lending issued during the pandemic is guaranteed by the Government, (ii) major UK banks and building societies (UK banks) have limited exposures to sectors with particularly low aggregate interest coverage ratios, and (iii) UK banks have made provisions for expected impairments on lending. Productive and viable businesses are likely to need continued support from the financial system as the economy recovers and the Government’s support measures unwind over the coming months. The UK banking system has the capacity to provide that support. It is in banks’ collective interest to support viable, productive businesses, rather than seek to defend capital ratios by restricting lending.

As set out by the FPC in July, some market asset valuations globally are elevated relative to historical norms. And terms on loans in global leveraged loan markets (in which UK banks and businesses participate) do not appear to reflect increased risks. This may indicate greater risk-taking behaviours by market participants. A sharp price correction could lead to other market participants – such as non-bank financial institutions – incurring losses. This could have consequences for market functioning and lead to tighter financial conditions for businesses. The FPC set out the next steps needed to enhance the resilience of market-based finance in July 2021, and strongly supports the work, co-ordinated internationally by the Financial Stability Board, to assess and where necessary remediate the underlying vulnerabilities.

Overall, the FPC continues to judge that the UK financial system is resilient to vulnerabilities in the UK corporate sector. But the evolution of vulnerabilities in the corporate sector will depend on the path of the economic recovery from the pandemic. The FPC will continue to monitor developments closely and remains vigilant to risks building up over the medium term.

1: The role of the FPC in monitoring risks from the UK corporate sector

This Financial Stability in Focus report provides a detailed assessment on how the Covid pandemic has affected UK businesses’ balance sheets and the implications for financial stability. The Covid pandemic and the measures taken to contain it have had a significant impact on UK private non-financial corporations (referred to as companies or businesses in this report). The support provided by the Government and financial system to help businesses weather the pandemic has increased the aggregate level of UK business debt. This has increased debt vulnerabilities moderately overall, but some sectors have been impacted more than others, as have SMEs relative to larger businesses.

This report will outline the FPC’s view of pre-Covid vulnerabilities for UK businesses, how they have changed over the course of the pandemic, and the FPC’s overall assessment of current risks.

The FPC aims to ensure the UK financial system is prepared for, and resilient to, the wide range of risks it could face — so that the system can serve UK households and businesses in bad times as well as good. A healthy business sector is important to a strong economy and well-functioning financial system over the long term. Consistent with the FPC’s primary objective of supporting financial stability, this means ensuring that any build-up of debt vulnerabilities in the corporate sector does not pose risks to the wider financial system, which could ultimately undermine the ability of the system to support businesses and households more broadly. Channels through which corporate debt vulnerabilities could impact the economy are set out in Figure 1 and include:

Losses to lenders and investors: large losses from businesses defaulting on their loans can threaten the resilience of lenders and providers of finance. This, in turn, could disrupt the supply of credit, particularly to riskier parts to the corporate sector. Business failures can also affect the ability of households to repay their loans if people become unemployed.

Borrower resilience: there is evidence that in an economic stress where credit is constrained, highly indebted businesses are more likely to cut their investment and employment by more than less indebted businesses. These behaviours can amplify macroeconomic downturns, leading to greater losses for lenders and affecting the provision of financial services.

Figure 1: A crystallisation of UK corporate debt vulnerabilities can affect UK financial stability

Consistent with its secondary objective to support HM Government’s economic policy, the FPC also considers the effectiveness of the financial sector in channelling finance to UK businesses and households. This includes understanding how, and for what purpose, businesses demand credit. The FPC is also concerned with how the financial system can best intermediate the supply of finance for productive investment. This can support the FPC’s primary objective of financial stability, and is important for long-term growth and productivity as part of the FPC’s secondary objective (see Box A).

2: The resilience of the UK corporate sector prior to the Covid pandemic

Prior to the Covid pandemic, the FPC judged that the UK corporate sector posed limited risk overall to UK financial stability, although there were pockets of risk. Prior to the Covid pandemic, total debt owed by UK businesses had been growing steadily. The corporate debt-to-earnings ratio stood at 322% in December 2019. While well below its peak in the global financial crisis of 377%, this measure had grown significantly from its post-crisis low of 279% in June 2015. This partly reflected strong issuance in the leveraged lending market: the FPC had been closely monitoring this and the accompanying loosening in underwriting standards – see the July 2019 Financial Stability Report (FSR).

Despite this increase in indebtedness, the UK corporate sector as a whole was resilient. Aggregate interest payments as a proportion of earnings were around historic lows, and profitability and liquidity positions were strong. Staff estimate that at the end of 2019, UK businesses’ profit margins, holdings of cash and equivalents and access to undrawn credit facilities could have absorbed a fall of 58% of turnover, even while paying labour costs in full. And the share of debt owed by businesses with high net debt as a proportion of earnings before interest and taxes (EBIT), had been broadly unchanged for many years (Chart 1).

Within that overall picture, however, there were some pockets of risk. In some industries – such as arts and recreation and utilities – the share of debt owed by businesses with high net debt-to-EBIT ratios were close to historic highs. While in aggregate UK businesses appeared liquid and profitable, only around a third of businesses held liquidity buffers that were larger than three months’ worth of turnover.

This reflected both that debt was more affordable in a low interest rate environment, and the resilience of the UK banking sector. Risks in the sector from increasing debt levels were limited by low borrowing rates. The share of businesses with low interest coverage ratios (ICRs)footnote [1] had been trending downwards steadily since the early 2000s, and had stabilised at historic lows in recent years, despite increases in corporate debt. And the Bank’s 2019 stress test showed that major UK banks and building societies (referred to as ‘UK banks’ hereafter) were resilient to losses on these exposures in a deep simultaneous recession in both the UK and global economies, combined with a significant fall in asset prices (see the December 2019 FSR).

Chart 1: There is a relatively large share of businesses with high levels of debt, but the share with significant interest burdens has fallen over time

Share of highly indebted businesses as measured by high net debt to earnings (left-hand panel) and low ICRs (right-hand panel), both weighted by debt share (per cent) (a) (b)

Footnotes

Sources: Fame (Bureau van Dijk), S&P Capital IQ and Bank calculations.

(a) High net debt to earnings defined as net debt to EBIT greater than or equal to 6. Low ICRs defined as below 2.5. Net debt to EBIT is calculated as total gross debt net of cash holdings as a share of the three-year moving average, where available, of earnings before interest and tax. ICRs are calculated as the three-year moving average, where available, of earnings before interest and tax as a share of interest expenses and interest capitalised.

(b) The largest listed companies are those with the highest three-year average turnover in a given year. The largest private companies are defined as those with turnover greater than £10 million in any given year.

3: The impact of the Covid pandemic on UK businesses’ indebtedness

The Covid pandemic was a substantial shock to UK businesses, but government support has helped to limit the impact of the economic disruption on UK businesses’ cash flows… The pandemic and associated public health measures led to a sharp fall in economic activity. While the impact has been uneven, almost all sectors saw a fall in gross value added in 2020 relative to 2019. UK businesses’ quarterly earningsfootnote [2] fell by around 9% in the first half of 2020, compared to 2019 Q4.

Government measures have provided material support over the past 18 months, limiting the impact of the pandemic-related disruption on businesses’ cash flows. For example, the Coronavirus Job Retention Scheme supported a cumulative total of 11.6 million jobs at various times by 16 August 2021, preventing a sharp rise in unemployment and also reducing businesses’ labour costs. UK businesses also received temporary relief in the form of VAT deferrals, a moratorium on commercial evictions, and a ban on winding-up petitions.

…and UK authorities took action to support the financial system in providing credit to businesses, with government-backed loans playing a particularly important role. UK authorities implemented measures to support banks in continuing to lend to businesses. In particular:

Businesses borrowed under the government-backed loan schemes – the Bounce Back Loan Scheme (BBLS), the Coronavirus Business Interruption Loan Scheme (CBILS), and the Coronavirus Large Business Interruption Loan Scheme (CLBILS) – all of which closed to new applications at end-March 2021. In total, the facilities approved loans worth £79 billion.

The Covid Corporate Financing Facility supported liquidity among larger businesses of investment-grade (or equivalent) standing, through the purchase of short-term debt. Prior to its closure to new purchases in March 2021, £37 billion had been lent to 107 businesses.

In addition, the Bank took action to support the financial system’s ability to provide credit to businesses during the pandemic. For example, the Bank’s Term Funding Scheme with additional incentives for SMEs offered eligible financial institutions the ability to access funding for four years at rates close to Bank Rate. And the FPC cut the UK countercyclical capital buffer rate to 0%, cancelling a planned increase to 2%, thereby reducing the amount of capital banks were required to hold, to support lending through this period.

In aggregate, corporate debt levels have increased moderately, although the increase in indebtedness has been more substantial in some sectors and for SMEs. Aggregate corporate debt increased by £79 billion to £1.4 trillion between end-2019 and 2021 Q1. Combined with a fall in earnings, this has increased the UK’s corporate debt-to-earnings ratio from 322% to 349% over the same period (Chart 2). Just over a quarter of this increase was driven by the fall in earnings and can be expected to unwind as earnings recover.

Chart 2: UK businesses’ debt-to-earnings ratio has increased over the pandemic

Sources: Association of British Insurers, Bank of England, Bayes CRE Lending Report (Bayes Business School (formerly Cass)), Deloitte, Eikon from Refinitiv, Financing & Leasing Association, firm public disclosures, Integer Advisors, LCD, an offering of S&P Global Market Intelligence, London Stock Exchange, ONS, Peer-to-Peer Finance Association and Bank calculations.

(a) These data are for private non-financial corporates, which exclude public, financial and unincorporated businesses. Earnings are defined as businesses’ aggregate gross operating surplus, adjusting for financial intermediation services indirectly measured.

The aggregate increase in debt has not been evenly distributed across businesses. Complete data on how company balance sheets have been affected will not be available until early next year. But data for large listed businesses – which account for nearly a quarter of turnover – suggest that they did not increase their debt significantly in 2020, and that the share of large listed businesses with ICRs below 2.5 was broadly unchanged in 2020 (Chart 1).

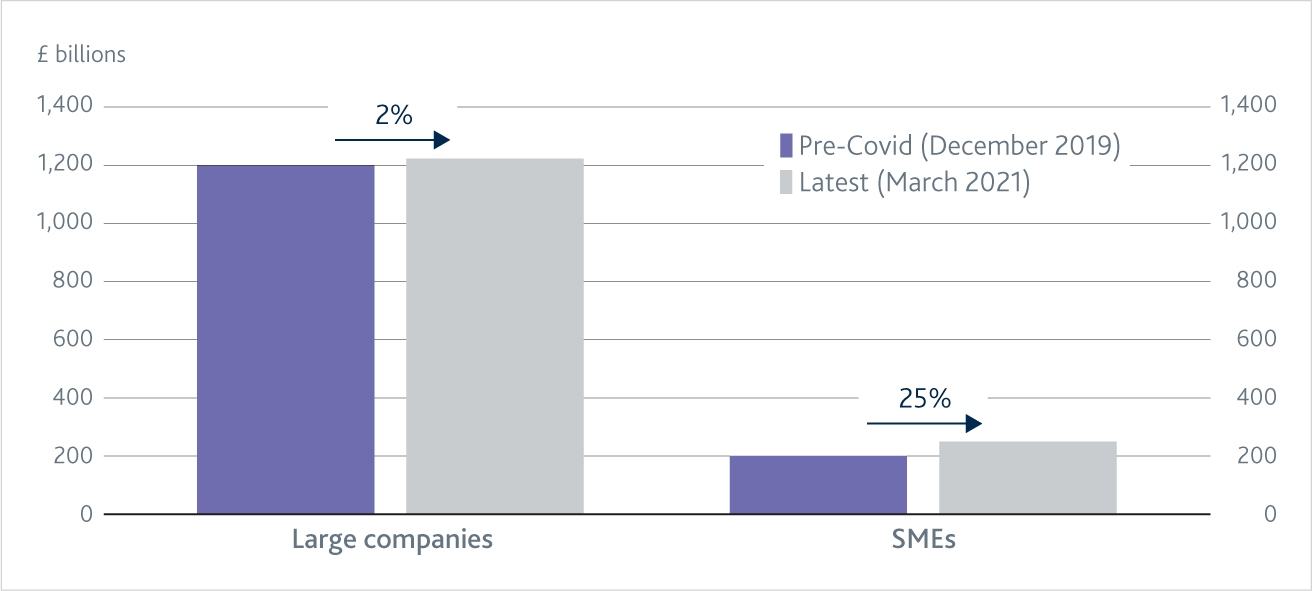

Chart 3: Growth in SME indebtedness has substantially outpaced that of larger businesses.

The increase in debt by type of size of borrower (a)

Footnotes

Sources: Association of British Insurers, Bank of England, Bayes CRE Lending Report (Bayes Business School (formerly Cass)), Deloitte, Eikon from Refinitiv, Financing & Leasing Association, firm public disclosures, Integer Advisors, LCD, an offering of S&P Global Market Intelligence, London Stock Exchange, ONS, Peer-to-Peer Finance Association and Bank calculations.

(a) These data are for non-financial businesses. SMEs are defined as companies with turnover of up to £25 million. Market-based debt consists of debt securities, including commercial paper, bonds, and private placements, as well as loans held by non-bank financial institutions.

However, the build-up in risk is likely to be particularly significant for SMEs: in total, SMEs’ outstanding gross debt increased by around a quarter between the end of 2019 and 2021 Q1 (Chart 3). Around two thirds of the increase in gross debt for the corporate sector as a whole is accounted for by SMEs, reflecting both the expansion in loan supply to SMEs via government loan schemes, and the fact that smaller businesses are most likely to operate in sectors affected by the Covid pandemic (see ‘How has Covid-19 affected small UK companies?’). SMEs in sectors particularly affected by the pandemic (such as arts and recreation, and accommodation and food) saw average debt increases of more than a third relative to their pre-Covid debt levels. These sectors were also more likely to take advantage of broader government support.

The unprecedented level of public sector support, as well as changes to insolvency legislation, have helped limit the number of businesses that have become insolvent during the pandemic (see Section 4.1).

And issuance through financial markets continued to be a significant source of finance for large listed businesses. A significant proportion of the increase in gross debt not accounted for by SMEs was driven by financial market issuance by larger businesses. In addition to debt-based finance, UK companies also raised substantial amounts of equity-based finance: gross equity issuance by UK businesses of £26 billion in 2020 was close to the record level of £31 billion in 2009, and almost three times the 2010–19 annual average of £9 billion.

When businesses with debt issue equity and reduce their overall leverage, they improve the resilience of their balance sheets, thus supporting financial stability. Staff analysis of a sample of large listed businesses shows that more than half of businesses with ICRs below 2.5 issued equity in 2020. Within that group, a third of businesses also issued additional debt.

These actions have helped improve businesses’ cash positions in aggregate. The combination of financing and government support has also led to an improvement in UK businesses’ aggregate liquidity positions. Overall, businesses’ cash balances have increased by £152 billion (or 29%) since end-2019. Just over half of this increase has come from external financing. Around half of SMEs held at least one month’s worth of turnover as cash reserves in May 2021, compared to 39% in the previous year. This suggests some of the borrowing was precautionary and may not have translated into increased vulnerability.

Despite the increase in debt in aggregate, a significant share of UK businesses did not take on new debt during the pandemic. As set out above, the increase in debt has been unevenly spread across UK businesses. Despite the availability of finance (including through government-backed loan schemes), the majority of businesses did not borrow during 2020. The £79 billion increase in aggregate debt is lower than Bank staff projections of the cash-flow deficits of the sector since March 2020.

This is likely to have reflected a number of factors. Companies with cash-flow surpluses are less likely to have needed to access external financing. Of those that did have deficits, some may have struggled to access finance on affordable terms, or may have preferred to meet their deficits in other ways than borrowing eg by cutting costs, drawing on cash buffers, selling assets or receiving capital injections from parent companies.

4: The FPC's assessment of the impact of the pandemic on corporate sector vulnerabilities

The evolution of vulnerabilities in the corporate sector will depend on the path of the economic recovery. Given the increase in indebtedness that has been observed to date, the FPC has examined the resilience of the financial system to risks linked to UK businesses. As shown in Figure 1, financial stability risks can arise from both the borrower resilience channel and through direct losses to lenders. The FPC has considered both the resilience of businesses to further shocks in earnings and interest rates (Section 4.1) and the potential for losses to lenders and risks in financial markets (Section 4.2).

4.1: Business indebtedness and resilience to further shocks

Debt servicing remains affordable for the majority of larger businesses. Debt-servicing costs are an important measure of vulnerability to shocks. A low ICR indicates that a company is more vulnerable to shocks that either increase its repayments (such as an interest rate increase) or lower its earnings. Staff analysis indicates that there is a turning point in the relationship between ICRs and the probability of company distress, with companies with ICRs below 2.5 materially more likely to experience repayment difficulties. And as businesses experience distress, they are more likely to take defensive action such as cutting spending (eg investment or hiring).

Over the pandemic, central banks have cut interest rates, quantitative easing has helped keep medium and long-term interest rates lower than they would be otherwise, and financial market conditions have remained accommodative. Despite increasing debt levels, the vast majority of new bank loans have been issued via government-backed lending schemes where terms were longer, and borrowing rates lower, than most businesses would otherwise have been able to obtain. And, as noted above, analysis of large listed businesses accounting for around a quarter of total UK business turnover shows the share of businesses with ICRs below 2.5 was unchanged in 2020 from 2019.

Large increases in borrowing costs would be needed to impair larger businesses’ ability to service their debt in aggregate… One of the factors that could affect debt affordability in the medium term is an increase in borrowing costs (for example, from credit conditions tightening or risk-free rates increasing). Chart 4 shows how the share of highly indebted borrowers (those with an ICR of 2.5 or lower) changes with increases in borrowing costs. Overall, borrowing rates would need to increase by as much as 200 basis points for the share of businesses with an ICR below 2.5 to reach levels seen at the time of the global financial crisis (or 400 basis points to return to its historical maximum) – though the sensitivity varies between sectors. This simulation is based on the assumptions that earnings remain flat (despite analyst expectations of earnings increasing) and that the increase in interest rates is immediately applicable to all debt. In practice, it would require interest rates to increase much more substantially to get a 200 basis points increase in borrowing costs, as a large proportion of the debt is at fixed rates or hedged. This means pass-through to corporate debt would take time, and businesses may be able to reduce their debt in the intervening period to reduce the impact of the rate rise.

Chart 4: A large increase in borrowing rates would be required to markedly increase the share of business with high debt-servicing costs

Share of businesses with ICRs below 2.5 for given increases in borrowing rates, weighted by debt share (per cent) (left-hand panel) and split by sector (right-hand panel) (a)

Footnotes

Sources: Bank of England, Fame (Bureau van Dijk), S&P Capital IQ and Bank calculations.

(a) ICRs, the largest listed UK companies and the largest private UK companies are defined as per Chart 1. Increases in borrowing rates are relative to end-2019. The sample includes non-financial corporates only, excluding those engaged in oil, gas and mining. Sector results, and the maximum historical share, are drawn from the sample of all listed UK companies and largest private UK companies.

…and severe earnings shocks would be needed to increase the share of businesses with ICRs below 2.5 to the levels seen at the time of the global financial crisis. A second important determinant in the assessment of debt affordability is earnings. A fall in earnings would reduce a business’ ability to make repayments on its debt. Analysts expect company earnings to substantially exceed pre-Covid levels by 2022 (Chart 5). Based on these expectations, the outlook for changes to earnings suggests widespread debt-servicing difficulties are not likely, although there is variation between sectors (Chart 6).

Chart 5: Analysts expect company earnings to exceed pre-Covid levels by 2022

Median expected change in earnings for listed companies relative to 2019 (a)

Footnotes

Sources: Eikon by Refinitiv and Bank calculations.

(a) Expected earnings are the median analyst forecast for EBIT in a given year, for a consistent sample of 395 non-financial corporates (excluding those engaged in oil, gas and mining). Forecast earnings are assigned to the calendar year in which the majority of the company’s financial year falls. Data up to 26 August 2021.

Very severe aggregate earnings shocks (eg a shock to EBIT of around 35%) would be required to return the current share of companies with low ICRs (37%) to the 51% seen around the time of the global financial crisis. However, it is likely that there would be significant dispersion within the aggregate, with some businesses experiencing larger falls. Earnings weakness may also be more persistent for those sectors most affected by structural change, precipitated or accelerated by the Covid stress. Using a similar approach, Bank staff have examined the impact of the pandemic on US and euro-area companies, including their ability to service their debt under shocks to borrowing costs or earnings (see Box B).

Chart 6: In most sectors, a severe earnings shock would be required to materially increase the share of businesses with high debt-servicing costs

Share of businesses with ICRs below 2.5 for given falls in earnings, weighted by debt (a)

Footnotes

Sources: Bank of England, Fame (Bureau van Dijk), S&P Capital IQ and Bank calculations.

(a) ICRs, the largest listed UK companies and the largest private UK companies are defined as per Chart 1. Earnings measured as EBIT, and changes are relative to end-2019. Sector results are drawn from the sample of all listed UK companies and largest private UK companies.

But within this aggregate picture, there remain some pockets of risk. The impacts of Covid have not been distributed evenly and it is likely that many businesses will have become more vulnerable. Businesses that are not able to adapt their business models to the structural changes brought on by Covid are likely to be particularly vulnerable. Uncertainty also remains over the outlook for the economic recovery. Earnings remain below pre-Covid levels in some sectors and challenges around supply chains, input cost inflation and labour shortages are currently putting some companies under pressure. This could have potential consequences for future earnings.

A subset of businesses were vulnerable prior to Covid, including a tail of highly leveraged businesses. The increase in indebtedness over the course of the pandemic is likely to have increased this tail further. This trend reflects supportive financing conditions in financial markets in the UK and globally, a trend that had been seen prior to the pandemic. As set out in Section 4.2, a tightening in financial market conditions could pose risks to some companies – particularly those that are highly leveraged.

Significantly more SMEs now have debt to service, and while the majority of new debt was relatively cheap due to government loan schemes, this will add to pressure on weaker SMEs. The Bank has acquired data on 2 million limited company SMEs.footnote [3] Staff analysis of these data shows that the share of SMEs with debt has more than doubled over the Covid period, with around 757,000 SMEs in the sample now holding debt. The vast majority of new debt has been issued at relatively low interest rates via government-guaranteed loan schemes.

Some of this increase in debt will have been for precautionary purposes. Currently 32% of limited company SMEs with debt in this data set have sufficient cash to repay all debts in full. However, some of these SMEs may be conserving cash surpluses for other obligations expected to fall due over the coming months (such as rent and VAT arrears repayments).

Most loans taken via government schemes have longer terms, cheaper borrowing rates and greater repayment flexibility than typical SME loans, which will support debt affordability among SMEs. Nevertheless, debt repayments are likely to be a drag on SME profitability for the foreseeable future. Around a third of SMEs have debt levels more than 10 times their cash balances, or are in their overdraft, and around a fifth have monthly debt repayments that are over 15% of their current account inflows (Table A). Around 10% of businesses fall into both these buckets.

Table A: There has been a substantial increase in the number of SMEs that now have debt

Proportion of limited company SMEs with high debt burdens (a) (b)

Number/percentage of businesses

Pre-Covid

Post-Covid

High debt to cash (greater than 10x, or already in overdraft)

14%

33%

High monthly payments to inflows (greater than 15%)

3%

18%

High debt to cash and high monthly payments to inflows

3%

10%

Total companies with debt post-Covid

Around 757,000 (Around 452,000 of which had no debt pre-Covid)

Footnotes

Sources: Fame (Bureau van Dijk), Regulatory reporting and Bank calculations.

(a) The data sample refers to limited company SMEs reporting non-zero debt post-Covid (after 1 March 2020). Due to data constraints, we cannot show ICRs for SMEs and therefore have presented alternative indicators of their increasing debt burden.

(b) The monthly loan payments during the post-Covid period are forward looking and incorporate the projected average monthly payment for scheme loans.

Although debt appears affordable in the near term, insolvencies are likely to rise from 2021 Q4 as government support is withdrawn as planned. Insolvencies have been limited during the Covid pandemic (Chart 7). But it is likely they would have been significantly higher in the absence of government measures (such as those mentioned in Section 3), support from the financial system and temporary changes to insolvency legislation including the restrictions on winding-up petitions which began to be relaxed from the end of September.

Chart 7: Insolvencies have been subdued during the Covid pandemic

Total quarterly number of new company insolvencies, 2006–21

Footnotes

Sources: The Insolvency Service and Bank calculations.

There have been at least 6,000 fewer insolvencies since the start of the Covid pandemic than might have been expected given the average level of insolvencies in the years leading up to the pandemic. Some of these may have been prevented altogether, but others are likely to materialise in the period ahead as support measures unwind, repayments on new borrowing begin, and other obligations postponed under deferral schemes – such as the VAT deferral scheme – become due.

And there is some early evidence of stress emerging. According to the latest BVA/BDRC SME Finance Monitor, 7% of all SMEs are concerned about their ability to make repayments, down from 10% in 2020 Q4 but still well above the pre-pandemic level of 4%. Concern about making repayments was found to be highest among SMEs that had either borrowed for the first time or had taken out new debt during the pandemic, mainly through the government-backed schemes. Sectors with the highest share of concerned borrowers included: manufacturing; hotels and restaurants; and transport, storage and communications. However, the major UK banks have not yet reported a material deterioration in the quality of their SME loan book.

4.2 Ability of the financial sector to support UK businesses

The UK banking sector remains resilient to losses associated with an increase in insolvencies. If insolvencies increase in the period ahead, UK banks may experience losses on their corporate credit books. However, a number of factors are expected to mitigate the extent of such losses:

The majority of new lending during the pandemic is guaranteed under government schemes, limiting direct losses for UK banks.

UK bank exposures to the most vulnerable sectors (ie those with low ICRs) are relatively small (for example, the arts and recreation sector).

UK banks have provisioned for losses across their loan books, on the basis of forward-looking assessments of the UK and global economic outlook. In 2020, UK banks provisioned for around £22 billion of aggregate credit losses over the course of the year. In 2021 H1, they released around £2.7 billion, reflecting the improved macroeconomic outlook, a perceived improvement in the credit performance of borrowers, and a reduction in the stock of unsecured lending balances.

Nevertheless, there could be some indirect consequences from businesses’ failures for banks’ retail loan books and the broader economy. For example, SMEs account for around half of UK employment. Significant business failures could result in loss of employment, and therefore income, for the household sector and result in impairments on their outstanding bank debts (eg mortgages and unsecured credit). This could also reduce business investment and slow the recovery, leading to stress for other businesses.

The FPC continues to judge that the UK banking system is resilient to risks from the UK corporate sector. The interim results of the 2021 Solvency Stress Test (2021 SST) supports the FPC’s judgement that the banking sector remains resilient to outcomes for the economy that are much more severe than the Monetary Policy Committee’s central forecast, and would be able to continue to support the real economy through new lending to viable and productive businesses.

The FPC also remains vigilant to the risks arising from fragilities in financial markets, including those related to corporate debt. There is evidence of increased risk taking in financial markets (see, for example, the July 2021 FSR and recent publications by other international regulators such as the Federal Reserve and the European Securities and Markets Authority), which could result in sharp price corrections, market dysfunction, and tighter financial conditions for businesses. Vulnerabilities in financial markets have the potential to generate losses for lenders and investors and amplify the impact of company distress on market functioning by reducing the supply of finance.

Investors in corporate bond markets (including non-bank financial institutions) may experience losses if the value of their debt investments fall in response to businesses’ distress, or in anticipation of future distress. If investors expect company defaults to rise, they are likely to increase the compensation they demand for exposure to credit risk, increasing businesses’ financing costs. And this may spread to other assets not directly at risk (such as higher-rated investment-grade corporate bonds) if risk appetites fall more broadly, precipitating further tightening of financial conditions.

A deterioration in the economic outlook could trigger downgrades among UK businesses. ‘Fallen angels’ – businesses that lose their investment-grade status – might pose financial stability risks if investors are forced to sell their holdings of downgraded bonds (eg due to mandates to only hold investment-grade debt, the risk of underperformance, or higher capital charges associated with lower-rate bonds). If this were to occur at sufficient scale, this could put unsustainable pressure on the high yield market, potentially impairing market functioning and borrowers’ access to capital. For example, businesses are unlikely to be able to issue bonds during a fire sale of existing debt securities.

The consequences of this ‘fallen angel’ risk were seen in corporate bond markets in the March 2020 stress. Sterling index funds sold over 90% of such downgraded bonds. Even investors that are not subject to the same forced selling pressures sold holdings: for example, insurers sold around 25% of their downgraded bonds.

The immediate risks relating to ‘fallen angels’ – as indicated by the value of BBB- bonds judged by credit rating agencies to be at risk of downgrade to high-yield within 90 days (those on negative watch) – have returned to around pre-Covid levels. But this risk remains elevated at a longer time horizon relative to the pre-Covid period: the value of sterling bonds judged by credit rating agencies to be at risk of downgrade up to two years in the future (known as being on negative outlook) is almost three times as high as at the beginning of 2020.

In leveraged loan markets, the trend of increased prevalence of looser underwriting standards has continued, which increases risks to end-investors. The post-global financial crisis trends of increased leveraged loan issuance (typically loans to non-investment grade companies that are highly indebted or are owned by a private equity sponsor) and loosening in underwriting standards in these markets (as set out in the December 2019 FSR) have continued. Leveraged lending flows globally are elevated relative to historical levels. Recent UK leveraged lending flows have in part been driven by a surge in private equity investment in UK businesses: 2021 private equity investment is on track to exceed its 2019 level, which itself was a strong year. In practice, UK businesses also issued in global markets (particularly the US).

The share of new lending in leveraged loan markets with few financial maintenance covenants has been growing since the global financial crisis, and gathered pace in particular since 2012. It now stands at around record highs in the UK and globally. Safeguards such as covenants provide lenders with additional protection, so the absence of such contractual provisions is expected to increase the risk of losses to end-investors. Should losses crystallise, there could be wider consequences for the supply of finance, as noted earlier. Some borrowers have benefitted from the additional flexibility during the pandemic, with fewer businesses that are viable in the long-term breaching covenants or having difficulty raising debt finance to bridge Covid-driven cash-flow deficits during the pandemic. But this may have led to some of these businesses taking on more debt than is sustainable, increasing their vulnerability to future stresses. Spreads on UK and global leveraged lending have largely returned to pre-Covid levels, suggesting they do not reflect these additional risks.

5: The FPC’s assessment of financial stability risks from the UK corporate sector

Overall, the FPC judges that UK corporate debt vulnerabilities have increased moderately in aggregate as a result of the Covid pandemic. UK businesses have so far weathered much of the disruption caused by the pandemic, with the support of government measures and loan schemes, and the financial sector. Vulnerabilities are moderately higher as a result of the increase in debt.

The path of earnings and borrowing costs will affect the affordability of this debt. In aggregate, most large UK businesses appear resilient to shocks to the cost of borrowing or to earnings.

The evolution of vulnerabilities in the corporate sector will depend on the path of the economic recovery from the pandemic as well as developments in financial markets. There is likely to be a larger vulnerable tail of businesses which are less able to weather a future shock than they were before the pandemic. It is likely that most businesses that were vulnerable prior to the Covid pandemic remain so today. In addition, new groups of vulnerable businesses have emerged as a result of the pandemic. SMEs are more indebted: staff estimates suggest 60% of those SMEs that now have debt did not have any before the Covid pandemic. Some of these SMEs may not have previously met banks’ lending criteria. And many of those who did have debt prior to the pandemic are now likely to have more. The outlook for these businesses will be heavily dependent on how economic conditions develop over the coming months. Some sectors remain at risk of an earnings recovery that is likely to be more protracted than the average for the corporate sector as whole – this limits their ability to withstand further distress in the future.

In addition to these groups of vulnerable businesses, the UK corporate sector is exposed to a tightening of conditions in financial markets. This can be seen most clearly in leveraged loan markets: the prevalence of lending at floating interest rates in this market in particular makes these borrowers more susceptible to risk from an increase in borrowing rates. However, while there are pockets of risk – such as in the leveraged lending markets – as the analysis in Section 4.1 sets out, a large increase in borrowing rates would be required for the share of all large business with high debt-servicing costs to return to its historical high.

Despite the moderate increase in vulnerabilities in the UK corporate sector, the FPC does not judge that this poses significant risk to the UK banking sector… Overall, the FPC judges that risks to major UK banks from direct losses associated with UK business defaults or distress are not likely to materially affect UK financial stability. This reflects the fact that virtually all of new lending by the UK banking sector since March 2020 has been under government-guarantee schemes, which will limit banking sector losses even in the event of business failure. Major UK banks have made provisions for potential losses based on forward-looking assessments of the outlook. And the banking sector remains well capitalised – a judgement that is supported by the interim results of the 2021 SST. The FPC therefore judges that the UK banking sector remains well placed to support the supply of credit to viable and productive UK businesses. It is in banks’ collective interest to support such businesses, rather than seek to defend capital ratios by restricting lending.

…however, the FPC remains vigilant to developments that might impact the economic recovery, or lead to a tightening in credit conditions. The evolution of the pandemic, and the responses to it, will continue to be an important driver of the economic outlook, which remains uncertain. In addition to the possibility of further restrictions, households and businesses may voluntarily restrict their activities in response to higher Covid cases in future. Supply constraints for businesses – as seen in recent months – may persist. And business distress could also translate into wider economic distress – for example, an increase in unemployment.

The availability of credit from the financial system has helped the UK corporate sector to weather much of the economic shock from the pandemic. However, if credit conditions were to tighten, this could present risks to the resilience of the UK corporate sector. Such risks could be exacerbated by vulnerabilities in market-based finance, such as those exposed in March 2020 (see Assessing the resilience of market-based finance), and the FPC strongly supports the work, co-ordinated by the Financial Stability Board, to assess and where necessary remediate the underlying vulnerabilities. The FPC continues to monitor credit conditions closely to ensure the financial system can continue to support UK businesses.

Box A: Productive finance: understanding the supply of finance to UK SMEs

The supply of finance including for productive investment is important both for financial stability and long-term growth. Addressing issues related to the supply of finance for productive investment (‘productive finance’) is an important aspect of the FPC’s remit. Productive finance is important to the FPC’s primary objective. Longer-term, less liquid and more equity-like investments can reduce leverage, redistribute risk across the economy, and can make the corporate sector more resilient to shocks, hence improving financial stability outcomes. Since 2015, HM Treasury has asked the FPC to consider how the financial system might best be able to intermediate the supply of finance for productive investment, subject to meeting its primary objective of maintaining financial stability. The effect of the pandemic on the UK corporate sector has brought into sharper focus the need to ensure that the financial system is able to intermediate the supply of productive finance to companies as the economy recovers.

In the UK, SMEs make an important contribution to the economy. But they experience more restricted access to finance. SMEs account for a substantial share of employment and turnover in the UK private sector, and represent a diverse range of businesses with varied financing needs. 60% of UK SMEs reported seeking external finance in the three years to 2020. There is evidence to suggest that reducing credit frictions to SMEs could improve medium and long-term growth (Besley et al (2020) and Samila and Sorenson (2011)). Some SMEs are more sensitive to economic fluctuations than larger companies, in part due to more constrained access to external finance (Davis and Haltiwanger (2019)). Improving access to finance for these businesses could make them more resilient and reduce the economic cost of business cycles.

When a business accesses external finance, the borrower usually knows much more about its creditworthiness than the lender does. This information asymmetry is more acute for some SMEs, such as newer businesses, which are less likely than more established companies to be able to show a credit history to demonstrate ability to repay debt. The absence of information is one of the reasons why lenders attach a higher risk premium to SME borrowers, and often require the loan to be secured against the SME’s assets. For prospective borrowers, the credit terms on offer shape their willingness to borrow and the form of financing that they take on.

In aggregate, the most significant form of external finance to SMEs is bank lending (Chart A). Prior to Covid, non-bank sources of debt finance to SMEs (eg peer-to-peer lending and asset finance) were growing as a share of total lending to SMEs. In 2020, after the pandemic hit the economy, SMEs’ reliance on finance from banks grew further.

But equity investment in SMEs has continued to increase steadily, from just under £4 billion in 2016 to £8.8 billion in 2020. This trend is important, because equity investment is an important feature of external finance for high-growth SMEs seeking to scale up rapidly. Those firms can provide an outsized contribution to growth in employment or productivity.

Chart A: UK SMEs face more limited access to finance than large companies, and access external finance primarily through bank lending

Composition of the stock of external debt finance to UK businesses (March 2021) (a)

Footnotes

Sources: Association of British Insurers, Bank of England, Cass Commercial Real Estate Lending Survey, Deloitte, Eikon from Refinitiv, Financing & Leasing Association, firm public disclosures, Integer Advisors, LCD, an offering of S&P Global Market Intelligence, London Stock Exchange, ONS, Peer-to-Peer Finance Association and Bank calculations.

(a) SMEs are defined as companies with turnover of up to £25 million. Data are as of 31 March 2021 or the latest available before then. Bank loans by ‘Large UK banks’ and ‘Other UK-based banks’ include lending to both private and public businesses. Bank lending may not cover some forms of financing, such as asset finance and asset-based finance provided through separate entities linked to banks. Debt securities includes bonds, private placements and commercial paper. Non-bank loans to large corporates includes lending by securities dealers and insurers, non-monetary financial institution syndicated loans, asset finance (lease and hire purchase) provided by the non-bank sector and direct lending funds.

Several recent government-led initiatives have sought to improve SMEs’ access to bank finance. Looking ahead, the focus continues to shift to facilitating access especially for more long-term, equity-like finance to high-growth and innovative businesses. Given the barriers that SMEs face in accessing finance, several government initiatives have been set up to address these barriers and better facilitate the supply of finance to SMEs.

In 2014, HM Government set up the British Business Bank (BBB) to increase the supply of credit to SMEs, primarily by providing lenders with government guarantees to cover a portion of credit losses on a portfolio and, in doing so, reducing the risk premium attached to lending to SMEs. Similar institutions have been long-established in other countries. The KfW Development Bank (KfW) in Germany, and the Small Business Administration (SBA) in the United States were set up following World War II to promote domestic industry, and have large balance sheets. For example, the KfW is one of Germany’s largest banks by balance sheet size. More recently, government-backed lending schemes in response to Covid have also increased the supply of finance to SMEs, which drew down approximately £70 billion across the BBLS and CBILS schemes (see Section 3).

Government-funded investment programmes delivered through British Patient Capital and British Business Investments (subsidiaries of the BBB) have already made progress towards addressing equity finance gaps for innovative companies. Proposals such as the Open Data Initiative could also allow SMEs to access a wider range of sources of bank and non-bank finance.

In addition, the Bank, HM Treasury and the Financial Conduct Authority have jointly convened an industry Working Group on Productive Finance. The aim is to develop practical solutions to barriers to investing in less-liquid assets, and in doing so, facilitate long-term investment into assets that expand productive capacity. In September, the Working Group published its final report supporting the need for long-term investments – such as investments in younger, smaller businesses with the capacity to grow – including via a Long-Term Asset Fund (LTAF). The report also sets out a roadmap of recommendations to removing barriers to long-term, illiquid investing. The FPC welcomes the Working Group’s report.

Understanding how the provision of finance to SMEs is developing is important for the FPC’s understanding of the vulnerabilities associated with SME indebtedness and for the FPC’s secondary objective, but is impaired by data gaps. The Bank will seek to address some of these gaps through a survey of UK businesses’ financing conditions in 2022. In 2017, the Bank published the findings of a Finance and Investment Decisions survey. A new survey by the Bank will supplement these findings. The survey’s sample will aim to be representative of the corporate sector, and compared with the previous survey, will aim to better represent SMEs, businesses at different stages of growth, and businesses which choose to take non-bank finance. The survey will improve the Bank and FPC’s understanding of the barriers to external financing that productive businesses face, and other factors that businesses consider in their financing decisions. The FPC welcomes the upcoming Bank survey on finance for productive investment.

Box B: Corporate debt vulnerabilities in the US and euro area after the Covid pandemic

Using a similar approach to the analysis of UK businesses, Bank staff have assessed the impact of the Covid pandemic on US and euro-area companies. As the UK has strong financial and trade linkages with the US and euro area, financial stress on US and euro-area companies could affect UK financial stability directly, via its impact on the quality of loans and other financial claims on those companies by UK financial institutions, and also indirectly, through the impact of slower economic growth in the UK’s trading partners on the UK economy. A tightening in financial conditions abroad can also spill over to UK financial conditions, including funding costs for banks.

In December 2019, the FPC identified elevated levels of corporate debt as a key vulnerability in the US and parts of the euro area. Since then, the Covid pandemic has been a substantial shock to the global economy. As in the UK, during 2020, corporate debt-to-GDP ratios increased, as GDP fell and firms took on more debt.

Like in the UK, US and euro-area policy responses were wide ranging. Governments and central banks introduced direct financial support to households, credit support to businesses and liquidity support to financial institutions. In the US and euro area, corporate bond issuance and net bank lending to corporates reached their highest levels in 2020 since the global financial crisis. This enabled companies to increase cash buffers, despite experiencing lower earnings.

Government support has now started to roll off in the US, and most government support is due to expire by the end of the year in the euro area. Once these schemes end, businesses may be exposed to higher financing costs, especially as government-guaranteed loans roll off. As noted by the Federal Reserve and the European Central Bank, these schemes particularly supported SMEs. Accordingly, risks will be heightened for SMEs, which typically experience more restricted access to capital markets and are therefore more vulnerable to a tightening in bank lending standards (see Box A).

The share of firms with an ICR below 2.5 had fallen in both the US and euro area since the global financial crisis, but that share has increased since the pandemic, driven by weaker earnings and increased debt.

Despite the economic shock from the pandemic, the shares of US and euro-area companies with a low ICR remain at the lower end of their historical ranges. It would require a shock of around 270 basis points in the euro area and 190 basis points in the US to bring the shares of firms with low ICRs to the top of the respective historical distributions. There can be large increases in risk premia, and borrowing rates, when a shock hits. A repeat of the shocks experienced during the global financial crisis, when euro-area and US corporate spreads increased by 360 basis points and 500 basis points respectively, would bring the share of US and euro-area firms with low ICRs significantly outside the historical ranges (Chart A). This is similar to the case in the UK, where increases in borrowing costs would have to be substantial to increase materially the share of corporates with an ICR below 2.5.

Chart A: Euro-area and US businesses’ borrowing costs remain at the lower end of the historical ranges

Sensitivity of firms with ICR below 2.5 to rises in borrowing costs, weighted by debt share (a)

Footnotes

Sources: S&P Capital IQ and Bank calculations.

(a) Historical distributions include data going back to 1996. Corporate spreads are calculated as the difference between a computed option-adjusted index of all investment-grade bonds and a spot risk-free rate. The ‘global financial crisis shock’ is calibrated from the trough-to-peak rise observed during the global financial crisis.

Similarly, a particularly severe shock to earnings would be required to push the debt share of firms with ICRs below 2.5 to the levels seen at time of the global financial crisis. However, as in the UK, the extent of the impact differs by sector. In sectors that may experience structural changes due to the pandemic, earnings weakness may be more persistent (Chart B).

Chart B: The impact of a shock to earnings on ICRs differs across sectors

Sensitivity of firms with ICR below 2.5 to weaker-than-expected earnings, weighted by debt share (a) (b)

Footnotes

Sources: S&P Capital IQ and Bank calculations.

(a) Energy and Utilities and Wholesale and Retail combine individual sectors due to differences between stress testing and standard industrial classifications.

(b) Shocks assume an identical reduction in earnings before interest and tax across sectors, all else equal.

The ICR is calculated by dividing a business’ EBIT by its interest expense during a given period.

Business earnings are defined as their aggregate operating surplus, as is the case in Chart 2.